Personal Capital is a tool that I use nearly every single day. Is it legit? Let's dive into our Personal Capital review to find out.

If you're a high-net-worth investor looking for ways to manage your assets, Personal Capital comes with an assemblage of features that sets it apart from other wealth management platforms.

Whether you're looking to put a finger on your financial accounts and save money, or if you’re seeking tailored recommendations to enhance your returns, this mobile and desktop-friendly platform aims to help you take control of your financial life.

Is Personal Capital legit? This Personal Capital review takes a deep dive into the platform’s pros, cons, capacities, and interface to help you in your quest for the best financial management tool.

I used to obsess over checking Personal Capital... Checking my net worth daily. It helped me clean up my personal financial situation. Share on X

I made the switch from Mint to Personal Capital and have been loving every minute of it.

It's no secret that it's one of my favorite financial resources and personal recommendations. Personal Capital can help you with your personal financial planning.

It's not for everyone though, so I wanted to provide a helpful guide to explain the differences and provide a full review of the Personal Capital platform.

If you’re considering Mint, we’ve also pitted the two against one another so you can make an informed choice.

Here’s everything you need to know to get started.

Table of Contents

What is Personal Capital?

Used by around two million people around the world, Personal Capital is a wealth management service founded in 2009 by Louis Gasparini, Rob Foregger, and Bill Harris in San Carlos, California.

Bill Harris, who was formerly the CEO of Paypal and Intuit, serves as the platform’s CEO.

The platform has over 165 million registered users, 18,000 of which use its paid version and contribute nearly $8 billion in assets under the company’s management.

How Does Personal Capital Work?

Personal Capital comes in two versions: a free planning tool called the Financial Dashboard and a paid version called Personal Capital Wealth Management. These are two related features, but each provides unique functions.

The free planning tool compiles data from all your financial accounts and provides recommendations to enhance your returns. No matter where you invest or bank, this free feature is definitely worth checking out.

Personal Capital Wealth Management, on the other hand, uses powerful automated investment tools with assistance from human management, offering a balance between automated suggestions and traditional human investment.

This service requires a minimum account size of $100,000 to use. With such steep requirements, this service is not for the saving and investment beginners.

Let's dissect each feature and talk about its features and requirements.

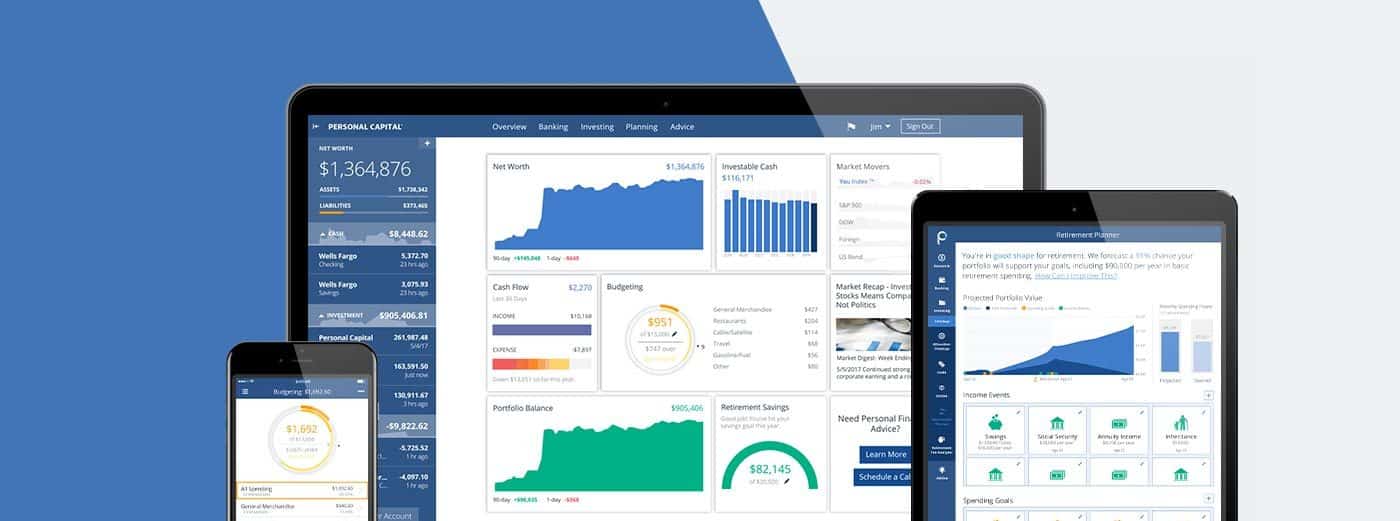

Personal Capital Free Dashboard

The free Financial Dashboard offers an extensive list of tools to help you budget your wealth and investments.

Primarily, this feature serves as a financial aggregator – you can use it to aggregate your checking, credit cards, loan accounts, savings, checking, and investments.

It’s built to put together your entire financial life in one platform. If you have any retirement plans sponsored by your employer, you can include it in the platform as well.

Let’s dissect each feature and outline the potential of each one:

-

Budgeting

The free version may be used to manage your spending and cash flow by showing monthly summaries that track where your money is going. Your spending is divided into trackable categories that you can analyze, along with your individual transactions.

If you’re aiming for budgeting software, Personal Capital underperforms in this respect.

While it does notify you of upcoming bills, the service does not include a bill payment function. This means that you have to pay your bills manually through your bank accounts.

See Related: Is It Worth it to Start Living Stingy?

-

401(k) Analyzer

If you're one of the millions of people who have signed up for employer-sponsored retirement plans, Personal Capital comes with a built-in feature that shows you how every fund in your plan costs you.

After it shows you the hidden investment fees associated with your plan, it then suggests alternative allocations into lower-cost funds.

-

Cash Flow Analyzer

This tool helps you manage your income and expenses from various financial accounts you've incorporated into the platform. After creating a budget, you can set financial goals such as paying off debt or preparing your retirement.

The analyzer will then suggest strategies for you to attain these goals.

-

Personal Capital Retirement Planner

By showing you several “what if” scenarios, Personal Capital helps you know if your retirement goals are still on the right track.

Use this feature to make adjustments to your situation, including the birth of a child, if you're saving up for college, or if you're making a career change.

The retirement planner then takes these outside factors into account to show you how it impacts your retirement.

-

Net Worth Calculator

Personal Capital’s net worth tracking tool helps track your liabilities and assets to show you your total net worth. This is integral to your financial status, as your net worth determines your financial strength.

This has been a complete gamechanger for me.

-

Investment Checkup

This is Personal Capital’s very powerful investment tool that helps you optimize your investments after you aggregate all your investment accounts into the platform.

It assists by making adjustments to your portfolio mix to enhance your investment performance.

-

Personal Advisor

Personal Capital’s free version comes with a personal advisor who can assist you with the platform’s service, as well as offer you additional insights on any recommendations made by the platform.

Know, however, that this advisor won’t be able to help you with investment advice.

Personal Capital Wealth Management

Personal Capital’s Wealth Management tool offers a mix of computer and human advice. While most of the services are automated investment tools, Personal Capital refuses to be classified as a robo-advisory service. Personalized advice from real financial planners offers a human touch.

Just like other automated investment tools, Personal Capital begins by analyzing your investment goals, risk tolerance, and time horizon.

The platform also takes into account your personal preferences in putting together your portfolio, which is managed according to Modern Portfolio Theory (MPT).

By applying MPT, your portfolio is invested across different asset classes for diversification.

Your portfolio is also rebalanced periodically to maintain target asset allocations.

There are six asset classes where your portfolio is invested. This includes:

- international bonds,

- international stocks,

- U.S. bonds,

- U.S. stocks,

- cash, and

- alternative investments, which includes gold, energy, and real estate investment trusts.

Depending on your investor profile, the percentage of your investment is divided into each asset class, as determined by your personal preferences, investment goals, time horizon, and risk tolerance.

Here are Wealth Management’s features:

Various accounts available: Wealth management offers the following accounts:

- Taxable and joint investment accounts

- SEP, traditional, rollover IRAs, and Roth

- Trusts

- 529 and 401(k) plans (advice only)

A designated accounts custodian: Pershing Advisor Solutions, one of the biggest clearing agencies and investment custodians in the world, is designated to hold your account. This company serves as a custodian for around $1 trillion in assets around the world.

Generous account protection: Signing up for Wealth Management guarantees protection from SIPC, with securities and cash up to $500,000, plus up to $250,000 in cash. The coverage provided only protects from broker failure, but not from monetary losses from market fluctuations.

Active financial advisors: Wealth Management’s main draw is its active financial advisors who you can keep in touch with 24/7, on email, phone, web conference, or live chat.

Two financial advisors will be at your disposal as a member of Wealth Management. You may consult with them regarding retirement planning, financial planning, college savings, and decision-making on topics such as home financing, compensation, insurance, and stock options.

Plans and fees: Personal Capital’s fees depend on the dollar value of the assets you have with them. There are three levels of asset management: Investment Service, Wealth Management, and Private Client.

Investment Service is the lower tier for users with $100,000 to $200,000 in assets. Wealth Management is the middle tier for users with investments between $200,000 to $1,000,000.

The highest tier is Private Client, for clients with $1,000,000 or more in assets.

Personal Capital Review: Personal Capital vs. Mint

Mint and Personal Capital both offer investment management and budgeting tools without fees (although the latter has a paid service called Wealth Management).

While the two are very similar, there are striking differences between both.

Budgeting

Mint rises to the occasion with its budgeting capabilities, as it is, first and foremost, a budgeting platform. Mint gives you a snapshot of all your finances so you can see the bigger picture, categorizes your spending, allows you to create a specific budget that analyzes your spending vs. your target, and offers alerts when your bills are coming in.

Personal Capital, which allows you to track your cash flow, offers budgeting capabilities but a more limited one.

Here is a full guide on how to use Personal Capital for budgeting in a step-by-step tutorial.

The verdict: Mint wins on this round.

Investments

Personal Capital shines when it comes to its investment capacities. Mint allows you to track your investment accounts but does not offer investment advice.

Personal Capital's paid Wealth Management service offers a bigger picture of your investment situation by working as an investment management service and a financial account aggregator.

The verdict: Personal Capital is the better choice for investment services.

Fees

Both Mint and Personal Capital are free services you can use to manage your finances. Personal Capital, on the other hand, has the bonus paid feature of Wealth Management that assists in managing your investments.

Personal Capital’s investment fees are all-inclusive, which means that it does not charge extra for account administration, commissions, or other associated investment fees. All fees under Wealth Management depends on the number of assets under management.

The verdict: Both have free services, so this is a tie. If you’re looking for an investment manager and you’re not afraid to shell out money, you might be better off with Personal Capital.

In summary, what is the better choice? The answer depends on what your goals are.

If you’re looking for a budgeting application without any additional features for investments, Mint is the better option.

If your needs lean towards investment management, Personal Capital’s wealth of features will better help you.

Personal Capital Pros and Cons Analysis

Before signing up for Personal Capital, you might want to know more about its upsides and downsides. Here’s everything you need to know before diving:

Personal Capital Pros

-

A free financial dashboard

Right off the bat, Personal Capital offers users a free financial dashboard that holds a wide array of budgeting features and investment tools.

The platform also offers investment advice even for accounts that are beyond your Personal Capital Wealth Management account.

-

Investment management and budgeting in one powerful platform

For users looking for a versatile platform, Personal Capital offers both investment management and financial management.

Beyond some of the already mentioned investment options, as a real estate investor, I love the ability to tack on my real estate assets. You can link this as your primary home too.

It's a great way to mark the valuation of your real estate over time.

-

Investments that are socially responsible

There are a growing number of investors who would like to make investments that are socially responsible and aligned with their values. Personal Capital does this by suggesting socially responsible investment opportunities.

-

Capacity to optimize your taxes

To help minimize the income taxes on all your investments, Personal Capital's Wealth Management program uses several tax optimization strategies

-

Help from financial advisors

Two financial advisors are assigned to each user in the Wealth Management platform. These virtual helpers can assist you in managing your financial life.

Personal Capital Cons

-

Some solicitation

Users signing up for Personal Capital’s free version might find the constant solicitation to upgrade to its Wealth Management service quite annoying.

-

Steep minimums

For the Wealth Management service, the initial investment requires is $100,000. This can make it difficult for entry-level and medium-sized investors to use.

-

Few budgeting features

As compared to apps like YNAB, Mint, and Quicken, which are purely dedicated to budgeting, Personal Capital offers limited budgeting capabilities.

-

Expensive fees if you use the robo-advisor

As opposed to robo-advisors like Wealthfront and Betterment that charge 0.25% to .40%, Personal Capital requires a fee of 0.89% for most investors.

This might be considered steep for users who often compare it to a mere robo-advisor.

However, Personal Capital offers investment management serves with a strong human touch, making it more akin to traditional human investment managers.

How to Sign Up for Personal Capital

Signing up for Personal Capital is a straightforward process.

If you’re also wondering how to link accounts to Personal Capital, here’s how to do it:

- Sign up through the website and provide your phone number and email. You will need to create a password.

- Provide your general information (age, name, your preferred retirement age, and how much money you have saved for retirement)

- Begin by linking your accounts. Personal Capital can link with more than 12,000 financial institutions, or you can also just enter the name and web address of your institution. The platform will then analyze your financial accounts from the past one to three months. Depending on this analysis, you will be given access to a variety of tools on the Free Dashboard, as well as offered recommendations for all of your investment accounts.

If you’re signing up for the Wealth Management service, here’s what you need to do:

- Get in touch with the platform’s financial advisor to begin. Additional information will be requested, as well as supporting documentation to officially verify your identity.

- You will also be asked to link your financial accounts into the platform so you can transfer funds to your Pershing account which will hold all your investments.

- You will need to answer a questionnaire and enter a web conference with a financial advisor to determine your investment goals, time horizon, and risk tolerance. Your portfolio will then be arranged depending on the findings.

Is Personal Capital Right for You?

If you’re looking for holistic help: Personal Capital is an attractive option for high-net-worth investors looking for a platform that operates as both an investment management service and a financial management service.

If you're looking for holistic assistance for your financial management, a mix of robo-advice and traditional consultants guarantees that you look at every element, and not just the sum of its parts.

If you’re only looking for a budgeting service: If you’re only on the lookout for a budgeting service, this platform may fall short. You might be better off signing up for Quicken, YNAB, or Mint.

If you don’t have enough money to invest: You need at least $100,000 to invest in Personal Capital’s Wealth Management Service. Users who do have the aforementioned amount to invest but are only looking for automated investment management might find better options with a robo-advisor platform.

If you’re looking for the help of real investment advisors: If you’re an investor who needs human help from trusted advisors, Personal Capital is a cost-effective solution. Traditional human investment advisors may charge anywhere between 1% to 1.5% just to manage your portfolio.

Personal Capital offers you human advice without having to pay those fees.

Conclusion on Personal Capital Review: Is It Legit?

Personal Capital is a tool that can help you get on the path to independent wealth. It's a great free resource for busy professionals. You can use it to simply become a better investor and saver while you go out and join the fine things in life.

I simply can't imagine a world without Personal Capital. I'd be lost. Be thankful for financial software like this that makes our day-to-day livelihoods better.

Related Reviews

Related Resources

- How to Save Your Money with a Purpose

- 70 Ways to Make Extra Money

- Real Estate Crowdfunding Guide

- Why Should We Save Electricity?

Personal Capital

Free

Pros

- Intuitive Dashboard

- Easy to Use

- Completely Free

- Automated Tracking (Net Worth & Cash Flow)

- Tax Optimization

Cons

- Minimums for Investing

- Limited Budgeting Options